E6S-019 Benefits Valuation Strategy - Financial Benefits Part 3B

I How to recognize hard, soft and cashflow benefits

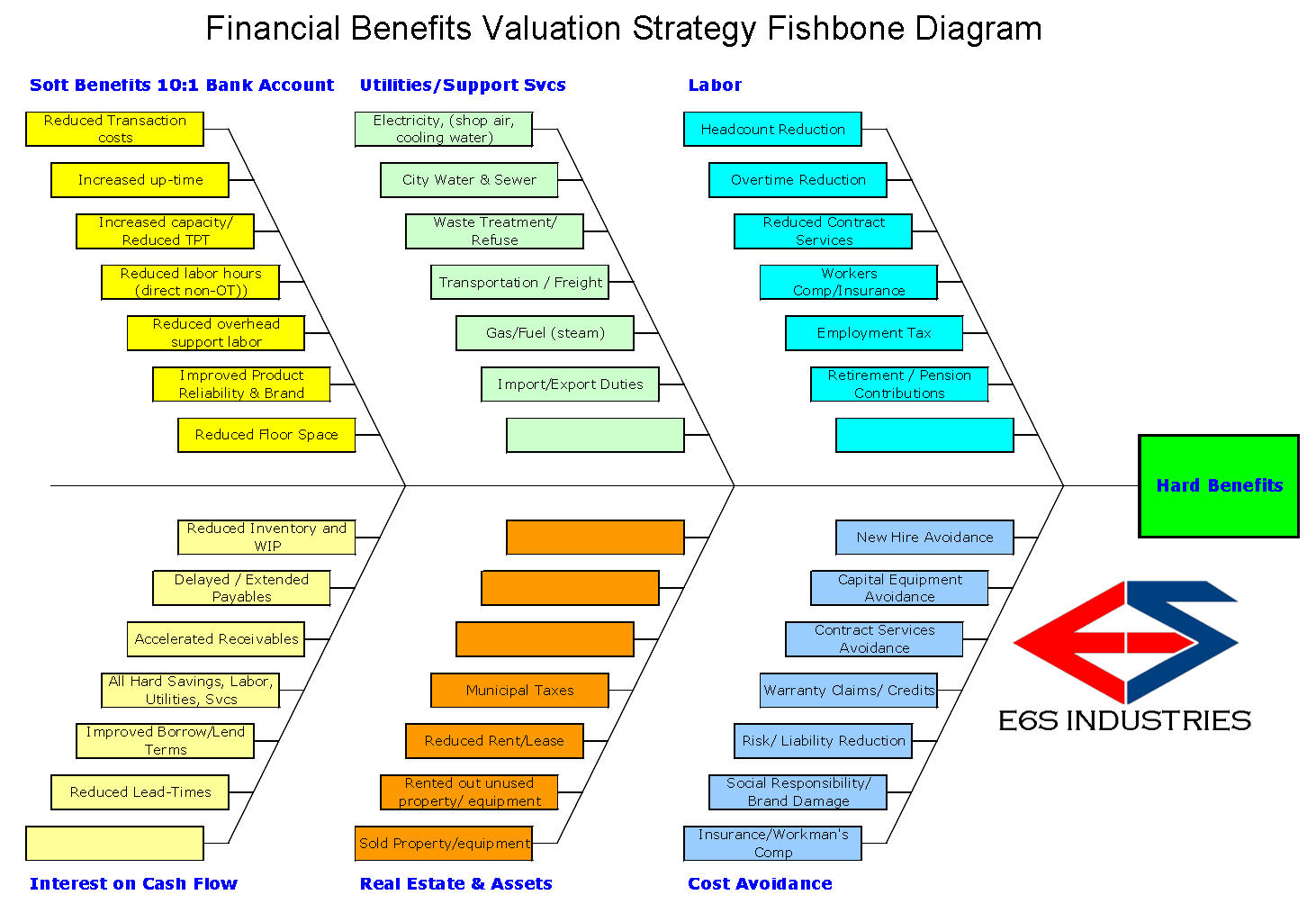

a. Fishbone

b. Practice: Projects to Critique:

i. World Leading Faucet Manufacturer – scrap reduction project

1. Project to reduce cost of scrap (COS) in plastic faucet production line. All defects resulted in scrap. No product could be reworked, and they were experiencing a high monthly scrap rate.

a. A successful BB project reduced monthly scrap from 14.5% to 12.2%. Financial Benefits Claims $18,000 monthly hard savings due to reduced scrap dollars or $215K scrap reduction annually. –

b. Sounds Great, right? ---Wrong. Many companies define their scrap dollars by their sales price. These scrap numbers are essentially lost sales, but actually translate into COPQ internal overage or OEE costs. There were no labor changes. True hard savings would have to be captured by a drop in OT, RM usage, waste & refuse costs, or greater sales if they met a new capacity (which they did.) The rest of the benefits are soft, and weren’t well captured. - CLAIMS REJECTED-

ii. Product Portfolio Consolidation Project – Huge savings claimed for eliminating dead weight product lines. Lets break it down.

1. Claim $375K annual in “Cost Avoidance”, $130K hard savings (interest on cash flow), (total hard benefits of $505Kand $620K cashflow reduction

a. Cost Avoidance Breakdown

i. Includes $128k in labor that would not need to be hired because, they are currently “overworked.” Who isn’t? - CLAIMS REJECTED-

ii. $247k in future scrap waste treatment that will not be necessary once everything is “cleaned up”. --- Park in Bank Account to watch. Could become real hard savings. ---

b. Hard Savings Breakdown

i. $75k in assumed eliminated over-time. Not measured. Assumed a 50% reduction. – CLAIMS REJECTED

ii. $45k interest on Cash Flow reduction. --- OK---

c. More Realistic savings to Claim:

i. $247K Soft Save Bank Account

ii. $45K Hard Benefits

iii. $650K Cash Flow Improvement

iii. Mama’s Soap Heals – Batches of soap were made in small batches, and sold in packs of 4 containers, ten 4-packs per batch. Each batch had leftovers equivalent to one full container, which was discarded.

1. A GB project was done to develop process that would allow containers of mixed lots to be sold in the same 4-pack. The heals were no longer being thrown away, but were being sold instead. The group claimed hard benefits of $3000 per month ($36k/yr) in profit enhancement, claiming the sales margins on the material that was previously discarded.

a. Sounds simple, right... they were once throwing it away, and now they are selling it. They claim the margins on increased sales. Open & shut... Not so fast. They didn’t actually increase the demand. Demand didn’t go up, so there was no increase of sales. Supply went up, an extra 4-pack per every 4 batches of soap produced (ten 4-packs each). Any hard savings would only be gotten after 40 full batches, which would save the purchase of one batch-worth of raw material. Also saved are the waste treatment costs of the soap, which was minimal. The major benefits were soft, and not well captured. - CLAIMS REJECTED-

iv. Chemical Batch Size Optimization –

1. A BB project to balance the cost of batch production with the with inventory holding costs. Claimed 260 reduced manufactured batches (same demand), $150K savings. But a net increase in inventory carrying cost of $44K (increased cash flow requirement).

a. Seems worth it. Spending ~ $3.5K in borrowing cost (interest on cash) to get a $150K return, right? --- Maybe. It depends

b. Consideration #1 – Despite the ROI math, can the company afford an additional $44K burden to cash flow? If not, this is a bad solution.

c. Where did the $150K come from? Was anyone let go? These were “cost avoidance” claims, due increasing plant production without increasing labor. (multi-plant consolidation). Very fuzzy category, not well traced to P&L.

v. Union Shop Aerospace– one extra blade kaizen –

1. Kaizen event to improve the throughput of turbine blades for jet engines. Kaizen team claimed an annual benefit of about $100k by being able to process one more blade per shift, equivalent to 21 extra blades processed per week (capacity enhancement). Clearly a “soft savings” by definition. Union shop, no change in labor

a. Great savings, right?.... Well..... The information missing from this, which was not presented at the Kaizen close-out was these blades were processed in batches of 6. The union culture was such that if you started the batch of 6, that was your batch, and no one else would touch it, so one extra blade processed meant the whole batch sat over night until the same operator picked it up and finished it the next day. They measured their own productivity by how many batches of 6 they processed. If they could not finish a batch of 6 before the end of the shift, they did not start it. Though I did not have the heart to interrupt this celebration at the Kaizen close-out, I knew there was literally zero savings from that project. It was only a “feel-good” exercise. - CLAIMS REJECTED-

vi. Defense Contract Nickel Plating Shop – Experienced low bath life and overall unpredictable plating bath control.

1. BB project to identify and control Critical X’s to adjust plating bath parameters to extend bath life (Metal Turnover’s) from 3.6 to 4.9 (i.e. 36% extension of life).

a. Project claimed a hard savings of $96k overall ($81k in reduced chemical usage, $9k reduced disposal cost, $6k reduced metal surcharge).

b. Pretty good, huh?.... YUP!.. Each of these savings was proven traceable to the P&L. These were real hard savings. What’s missing are the soft savings associated with reduced bath change-over labor costs, reduced Cash Flow for average chemical inventory, decreased defects due to better process control.. This project showed hard benefits, and more.

III Leaders expect some level of business savvy from project managers